The Business Case for Displacing Diesel

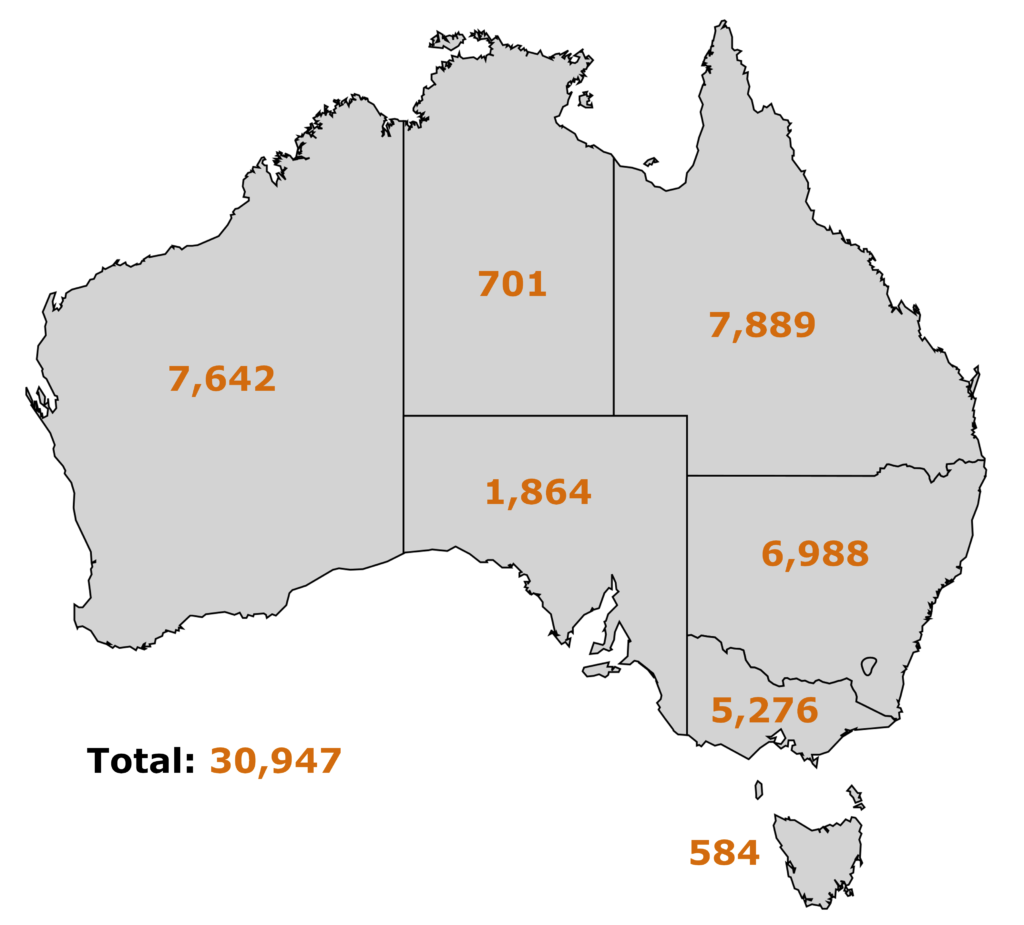

In 2021, Australia consumed around 31 billion litres of diesel fuel. For many businesses that consume large quantities of diesel across mobile fleets, displacing diesel for a lower cost and cleaner energy source presents an opportunity to create a climate advantage.

This article makes the case for businesses to evaluate diesel displacement strategies.

CY21 Diesel

(Million Litres Sold)

1. Energy Cost Certainty and Mitigation Exposure to Policy Change

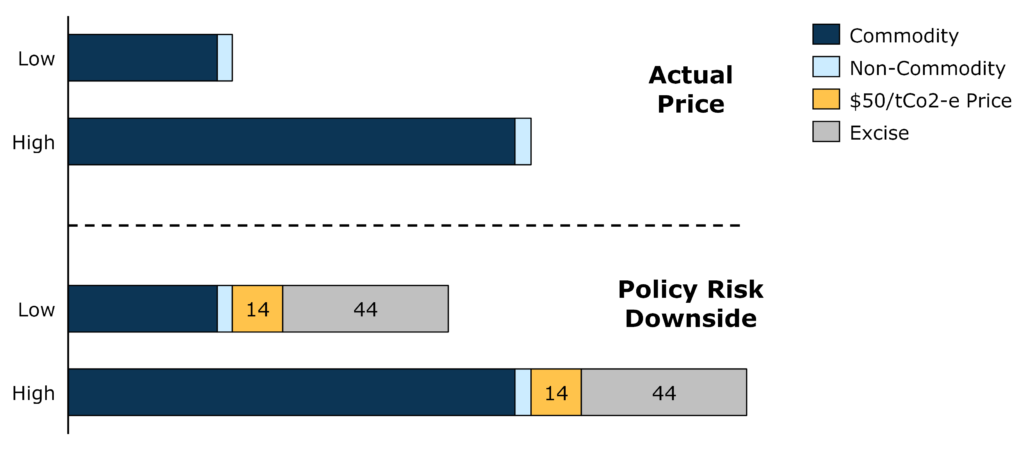

The chart below shows the high and low ex-terminal, pre-GST diesel price in Australian Cents Per Litre (ACPL) over the past 24 months (excluding April 2020 as an outlier due to the COVID-19 price shock).

Note that the underlying commodity price is the key driver in diesel cost. The non-commodity components of ocean freight, insurance fees, domestic port wharfage and terminal fees typically account for less than 10% of the overall price.

Challenge 1: High Price Variability:

The price of diesel is highly volatile. Over 24 months to

March 2022, the difference between the low and high price is a factor of

roughly 3x.

Challenge 2: Potential Macro Policy Changes Increasing Prices:

There are two key policy risks which threaten to

significantly increase diesel prices.

- A reduction in Fuel Tax Credit. Industries that consume diesel

outside of public roads (such as mining), are rebated 100% of the paid fuel

excise as a Fuel Tax Credit. Currently, the Fuel Tax Credit is 44.2 ACPL. - Introduction of a Carbon Price. An A$50/tCo2-e carbon

price will increase the price of diesel by approximately 14 ACPL.

These challenges can be mitigated by displacing diesel consumption with alternative fuel sources that have lower, more predictable pricing, as well as reduced emissions.

2. Decarbonising Operations

Options to economically decarbonise diesel fleets are rapidly becoming commercially advantageous. As a result, these alternatives are becoming key pillars of decarbonisation roadmaps.

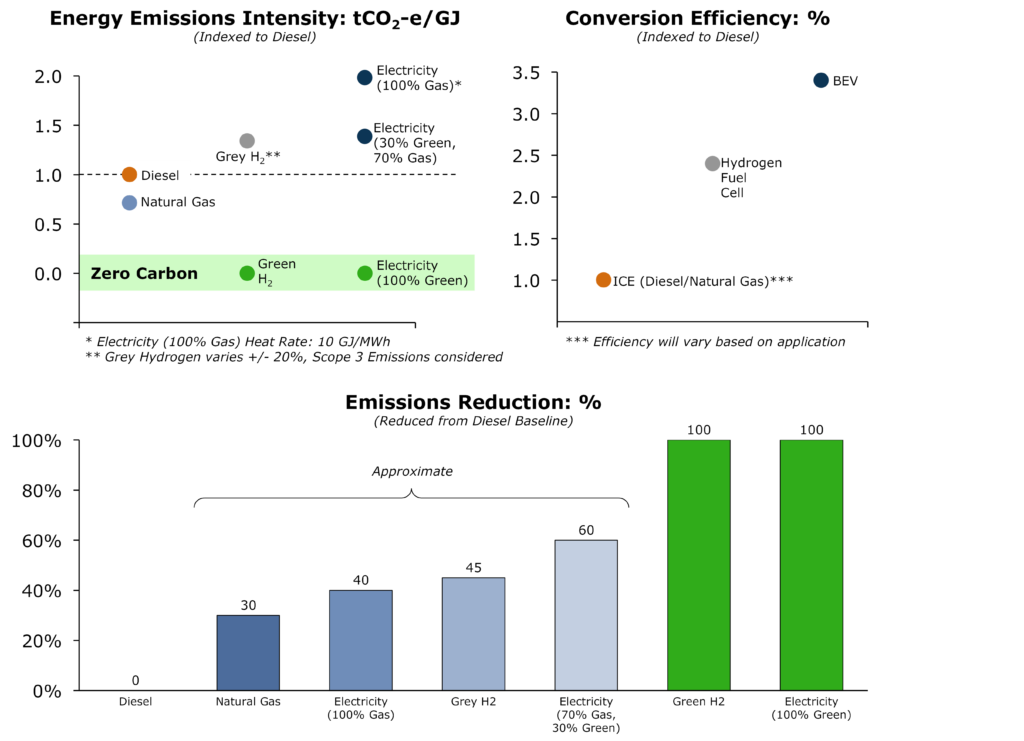

The effective reduction in emissions relative to diesel consumption is determined by two key variables:

- The delta in energy emissions intensity (the cleanliness of the energy source); and

- The delta in conversion efficiency (the efficiency at which the potential energy in the energy source is converted into usable energy).

On the first variable, it is important to understand that relative to diesel, on a tCO2-e/GJ basis, many energy sources are more carbon intensive. These include grey hydrogen and electricity generated using gas. For example, electricity generated using 70% gas and 30% renewables has ~1.4x the energy emissions intensity of diesel per gigajoule.

This is where the second variable becomes crucial. Consider that when consumed in an internal combustion engine (ICE), most of the energy contained in diesel is converted to excess heat and mechanical friction (i.e. wasted).

In comparison, hydrogen fuel cells and electric motors convert more of the potential energy into useful kinetic energy. Compared to an ICE, a hydrogen fuel cell is around 2.5x more efficient, and a battery electric vehicle (BEV) is around 3.5x more efficient.

Accordingly, emissions will be reduced when displacing diesel, provided the benefits from increased energy conversion efficiency outstrip the increased carbon intensity of the alternative energy source. As an example, electrifying a fleet even with electricity supplied by 100% gas generation still delivers around a 40% reduction to emissions. The 2x increase in carbon intensity is outweighed by the 3.5x improvement in energy conversion. As the electricity source becomes less carbon intensive, the overall emissions reductions increase. A zero-carbon fleet will only be possible, however, with zero-carbon fuels such as green hydrogen or 100% renewable energy generation.

3. Energy Cost Savings

Even putting aside emissions considerations, the energy cost savings from displacing diesel are material and growing as the cost of alternative energy forms rapidly decline thanks to the continually improving economics of renewable energy. It is not uncommon to experience over 80% reductions in the total cost of fleet energy from electrifying diesel fleets.

The principles and methodology outlined in section 2 hold true for cost, that is, they can be applied by substituting carbon intensity for cost:

- The delta in energy cost (the cost of the energy

source); and - The delta in conversion efficiency (the efficiency at which the potential energy in the energy source is converted into usable energy).

At a diesel price of $1/litre, the cost of energy is ~$26 per Gigajoule of energy. A $60/MWh power price, which is achievable across Australia with renewable energy, is equivalent to an energy cost of ~$17/Gigajoule. This delta in energy costs produces a saving which is further magnified as consumption via electrification is around 3.5x more efficient than consumption via an ICE.

At these prices, we would anticipate a reduction in total energy costs (diesel + electricity) of approximately 80%.

Conclusion

Businesses will be required to navigate the transition of fleets away from diesel to lower cost and cleaner energy sources, and this represents an opportunity to create a climate advantage supported by commercial decision making for those that evaluate diesel replacement strategies now.

If you would like to better understand the emissions landscape, calculate your own emissions and plan your decarbonisation journey, Mainsheet would welcome the opportunity to discuss it with you. Please contact us here.